Question:

Interpreting the statement of cash flow relations. Exhibit 6.34 presents statements of cash flow for eight companies for the same year:

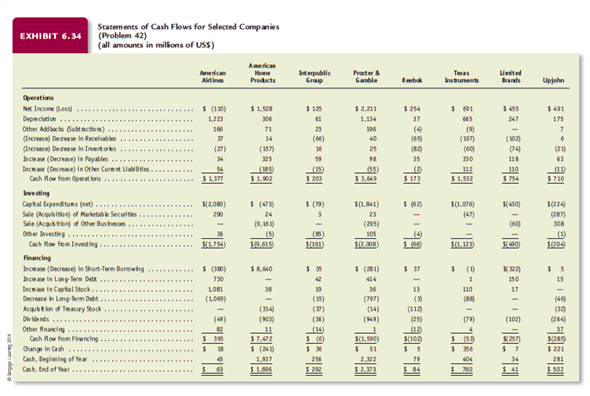

a. American Airlines (airline transportation)

b. American Home Products (pharmaceuticals)

c. Interpublic Group (advertising and other marketing services)

d. Procter & Gamble (consumer products)

e. Reebok (athletic shoes)

f. Texas Instruments (electronics)

g. Limited Brands (speciality retailing)

h. Upjohn (pharmaceuticals)

Discuss the relation between net income and cash flow from operations, and the pattern of cash flows from operating, investing, and financing activities for each firm.

Answer:

Step: 1 of 14

Identify the relation between operating cash flow and net income for the given eight companies, and explain about three sections of the statement of cash flows:

Cash flow statement:

Cash flow statement is one of the important and mandatory reports from the company’s financial reports. Cash flow statement records the transactions, which are related to cash, and cash equivalents.

It shows how cash is coming into the company and how it is going; and it will be prepared for one particular accounting period. This statement is divided into three parts operating, investing, and financing.

Step: 2 of 14

Three activities of statement of cash flows:

Operating activities:

• In this section includes items, which are related to expenses, revenue to identify net income of the company for a period.

• Cash flow from operating activities normally generates positive cash flow from operations. A negative cash flow from operations is a sure indicator of financial trouble.

Investing activities:

• Purchase or sale of assets includes in the cash flow from investing activities section.

• Investments made to purchase shares of other company are also part of investing activities.

• Cash flow from investing activities normally generates negative cash outflows as companies use cash to expand long-term assets.

• A company with positive cash flows from investing activities is selling off its long-term assets faster than it is being replaced.

Financing activities:

• Financing activity involve the receipt of cash, which include cash received from issue of common stock, loan taken from bank and the payment of cash to owners and creditors, which may include cash dividend paid or bank loan repaid.

• Further payment made to reacquire stock (treasury stock) or to payment made for bonds retired are also parts of financing activities.

• Cash flow from financing activities can generate either positive cash inflows or negative cash outflows.

• Positive cash flows from financing activities can be a sign of a young company that is expanding so fast that operations cannot provide enough cash to finance the expansion.

• Negative cash flows from financing activities might be exhibited by a mature company that has reached a stable state and has surplus cash from operations that can be used to repay loans or to pay higher cash dividends.

Step: 3 of 14

a) For AA Ltd., the high level of net loss is because of high depreciation charges. It has a moderate working capital requirement, however, has a very high depreciation charges. This high depreciation is confirmed by new capital expenditure that the company has made and probably is yet to receive any economic benefit out of it.

Step: 4 of 14

The company has entered into an expansion mode, highlighted by its new capital expenditure. At the same time, it is changing its capital structure by partially decreasing its debt and issuing fresh stocks. In comparison to other businesses AA Ltd. is better positioned and is expected to have further growth.

Step: 5 of 14

b) AHP Co. has a net working capital requirement of $(3), which is good. The company is efficiently maintaining its cash flows on current assets and liabilities to maximize cash from operations.

Step: 6 of 14

The company has distributed a large part of it net income to its shareholders. It seeks to increase its market value, boosting investor’s confidence. Reflecting a well-established position with high net income and cash balance, AHP is seeking expansion and further growth by investing in new businesses. When compared to other companies it is showing better performance than most of them.

Step: 7 of 14

c) IG Inc. with a working capital requirement of $(6) is at a moderate scale of business. It has a strong cash balance and has just started to invest in capital assets. It has used various sources of finance to expand further.

d) GP Co. has made high profits, which however includes a depreciation charge of $1,134. The high depreciation charge is validated by new capital expenditure which the company expects to utilize for future earnings. Its cash from operations includes a net working capital of $108, resulting in cash inflow.

Step: 8 of 14

Having sizable revenue, it is better positioned than all the other companies. It has strong working capital position, high profits and a very strong free cash flow. It further seeks to grow by fresh capital expenditure and acquisition.

Almost all the cash from operations have been used in business, probably because the company already has fat cash balance. It has improved its outside liabilities substantially, while paying a high dividend at the same time.

Step: 9 of 14

e) RE Ltd. seems to be caught in working capital problems, because the company has about half of its net income consumed in meeting working capital requirements, resulting in cash flow lower than the net income.

Step: 10 of 14

The company seems to have reached its peak of growth. Its working capital requirement is high resulting in outflow of cash, arising from pending receipts and unsold inventory.

It has not made any substantial investments. A large cash outflow is reported by buy-back of shares.

Step: 11 of 14

f) TI Corp. has depreciation expense higher than the net income, signifying healthy revenue. The depreciation is resulting from new capital asset acquisition made during the year.

One notable aspect of its cash flows is high net income still stuck in receivables. However, the company seems to have similar relation with its creditors as well, because it has high payables as well.

Step: 12 of 14

One of the promising companies of the eight, TI Corp. has a positive free cash flow, even after a high expenditure on capital investment. Its working capital position is very strong, allowing it to make optimum utilization of cash from operations.

It is notable that the company had financed its investment from within. Some fresh equity capital raised is almost nullified by debt repayment.

Step: 13 of 14

g) Reflecting a positive inflow from working capital, LLB is generating cash flow from operations higher than its net income. The company is in its initial stages of growth, visible by modest income and considerable capital investment.

Generating free cash flow sufficient to pay off short-term borrowings and pat dividends, it acquired long-term debt only to partially finance it capital expenditure.

Step: 14 of 14

h) U Inc. with a net income of $491 is doing stable and constant business. The company seems to be going through regular growth recently, reflected by high dividends payment. It is still considering further expansion by making a fresh capital investment.

I’m sourav, from Kolkata. A tech lover and love to answer any tech-related queries. I just try answering all questions like my problem.